%20Who%E2%80%99s%20Really%20Saving%20with%20Employer%20Student%20Loan%20Repayment%20Programs.png)

Employer Student Loan Repayment Assistance (SLRA) programs have quickly become one of the most talked-about financial wellness benefits. With student debt affecting millions of employees across industries, offering direct repayment support signals that employers are listening.

But as more vendors enter the market, a new question is emerging:

Are all SLRA programs created equal?

While many solutions help employers contribute funds toward employee loans, the structure behind the benefit can dramatically affect real employee savings, compliance risk, and long-term impact.

Let’s take a closer look at the key differences in vendor approaches—and who truly benefits most.

Key Takeaways

- SLRA vendors vary significantly in service depth, from basic payment processing to comprehensive borrower coaching.

- Employee savings increase when employer contributions are paired with personalized repayment strategy.

- Compliance with Section 127 tax rules and federal loan regulations is critical to protecting both employer and employee value.

- Programs that integrate coaching and automation tend to reduce HR workload while increasing employee engagement.

- The most impactful SLRA programs focus on optimization—not just disbursement.

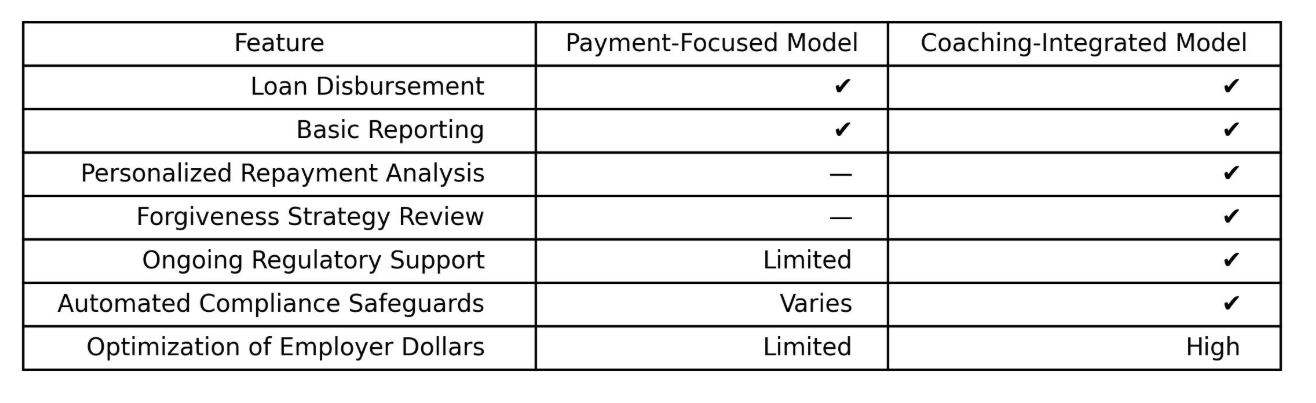

Two Common SLRA Vendor Models

When evaluating Employer Student Loan Repayment Assistance providers, most solutions fall into one of two broad categories:

1️⃣ Payment-Focused Platforms

2️⃣ Strategy & Coaching-Integrated Solutions

Both models enable employers to contribute toward employee student loans. However, how those contributions translate into savings can differ significantly.

Model 1: Payment-Focused SLRA Platforms

This model emphasizes administrative simplicity. Employers set a contribution amount, and the vendor facilitates payments to loan servicers.

What This Model Typically Provides:

- Automated loan disbursement

- Employer contribution tracking

- Basic reporting dashboards

- Payroll coordination

- Section 127 eligibility structure

Where It Delivers Value:

- Straightforward program setup

- Minimal operational lift for HR

- Clear, predictable budgeting

- Easy-to-understand employee benefit

For some organizations, this approach is sufficient—particularly when the goal is offering a competitive perk without adding complexity.

Where Savings May Plateau:

Student loan repayment is rarely “one size fits all.” Without personalized guidance, employees may:

- Remain on suboptimal repayment plans

- Miss eligibility for forgiveness programs

- Fail to adjust repayment strategy after life changes

- Direct employer contributions inefficiently

In these cases, the benefit reduces principal—but may not maximize total financial impact.

Model 2: Strategy & Coaching-Integrated SLRA Solutions

This model combines employer contributions with individualized borrower support and automated compliance oversight.

Instead of focusing solely on payment transfer, it asks a deeper question:

How can we optimize every dollar contributed?

What This Model Typically Includes:

- 1:1 borrower coaching

- Repayment plan analysis

- Forgiveness qualification review (e.g., PSLF, IDR)

- Ongoing regulatory guidance

- Automated Section 127 compliance management

- HR reporting and administrative support

How This Impacts Real Savings

When employer contributions are layered on top of an optimized repayment strategy, the financial results can compound.

For example:

- An employee shifting from a standard plan to an income-driven repayment plan may reduce monthly out-of-pocket payments while applying employer funds toward principal.

- A public sector worker correctly working towards PSLF can preserve eligibility while leveraging employer contributions to lower their monthly out of pocket payment.

- An employee refinancing high-interest private loans can accelerate payoff while lowering total interest costs.

In these scenarios, the employer contribution remains the same—but the total savings increase due to strategy alignment.

The Compliance Factor: An Overlooked Differentiator

Section 127 of the IRS code allows employers to contribute up to $5,250 annually tax-free toward student loans.

However, proper documentation, payroll coordination, and tax reporting are essential.

Vendor capabilities in compliance may include:

- Automated tax documentation

- Ongoing monitoring of legislative updates

- Structured reporting safeguards

- Integrated payroll validation

For employers, this reduces risk exposure and administrative strain. For employees, it protects the tax-advantaged value of the benefit.

Real-World Impact: What Employees Experience

When SLRA is paired with strategic guidance, employees often report:

- Reduced monthly out-of-pocket payments

- Faster payoff timelines

- Greater clarity around forgiveness programs

- Increased confidence in financial decisions

Anonymous employee feedback commonly reflects themes like:

“I didn’t realize changing my repayment plan would make such a difference alongside the company benefit.”

“The employer contribution helped—but understanding my strategy changed everything.”

Beyond financial savings, employees frequently cite reduced stress and stronger appreciation for their employer’s investment.

Comparing the Long-Term Value

Both approaches serve a purpose. The difference lies in how much value is unlocked from each employer contribution.

What Employers Should Consider

When evaluating SLRA vendors, organizations may want to assess:

- Is the goal to offer a competitive benefit—or to maximize measurable employee savings?

- How much guidance will employees need to navigate federal and private loan complexities?

- Does HR want a purely transactional solution—or a strategic financial wellness partner?

- How important is automated compliance and legislative monitoring?

The answers to these questions often determine which vendor model aligns best with organizational priorities.

The Bigger Picture: From Benefit to Financial Wellness Strategy

Student loan debt impacts retention, recruitment, and employee financial stress levels.

An SLRA program can be a powerful differentiator—but its impact depends on execution.

Payment processing delivers value.

Strategic guidance multiplies it.

When employer contributions are combined with coaching, regulatory oversight, and repayment optimization, the benefit becomes more than a line item—it becomes a measurable financial advantage for employees.

%20From%20Data%20Overload%20to%20Action%20Using%20Workforce%20Analytics%20to%20Target%20Financial%20Wellness.png)

%20123%20Is%20the%20PSLF%20Buyback%20Really%20Working%20What%20Borrowers%20Need%20to%20Know.png)